All Categories

Featured

Table of Contents

Added amounts are not ensured beyond the period for which they are stated. Converting some or all of your cost savings to earnings benefits (referred to as "annuitization") is an irreversible decision. When revenue benefit repayments have actually begun, you are unable to transform to one more option.

These extra amounts are not assured beyond the duration for which they were declared. These computations use the TIAA Conventional "new money" revenue rate for a solitary life annuity (RUN-DOWN NEIGHBORHOOD) with a 10-year warranty duration at age 67 making use of TIAA's basic settlement method beginning income on March 1, 2024.

The outcome ($52,667) is initial earnings for Individual B in year 1 that is 32% greater than the initial earnings of Participant A ($40,000). Revenue prices for TIAA Standard annuitizations are subject to change regular monthly. TIAA Traditional Annuity income benefits consist of assured amounts plus added quantities as may be declared on a year-by-year basis by the TIAA Board of Trustees.

Annuities 10

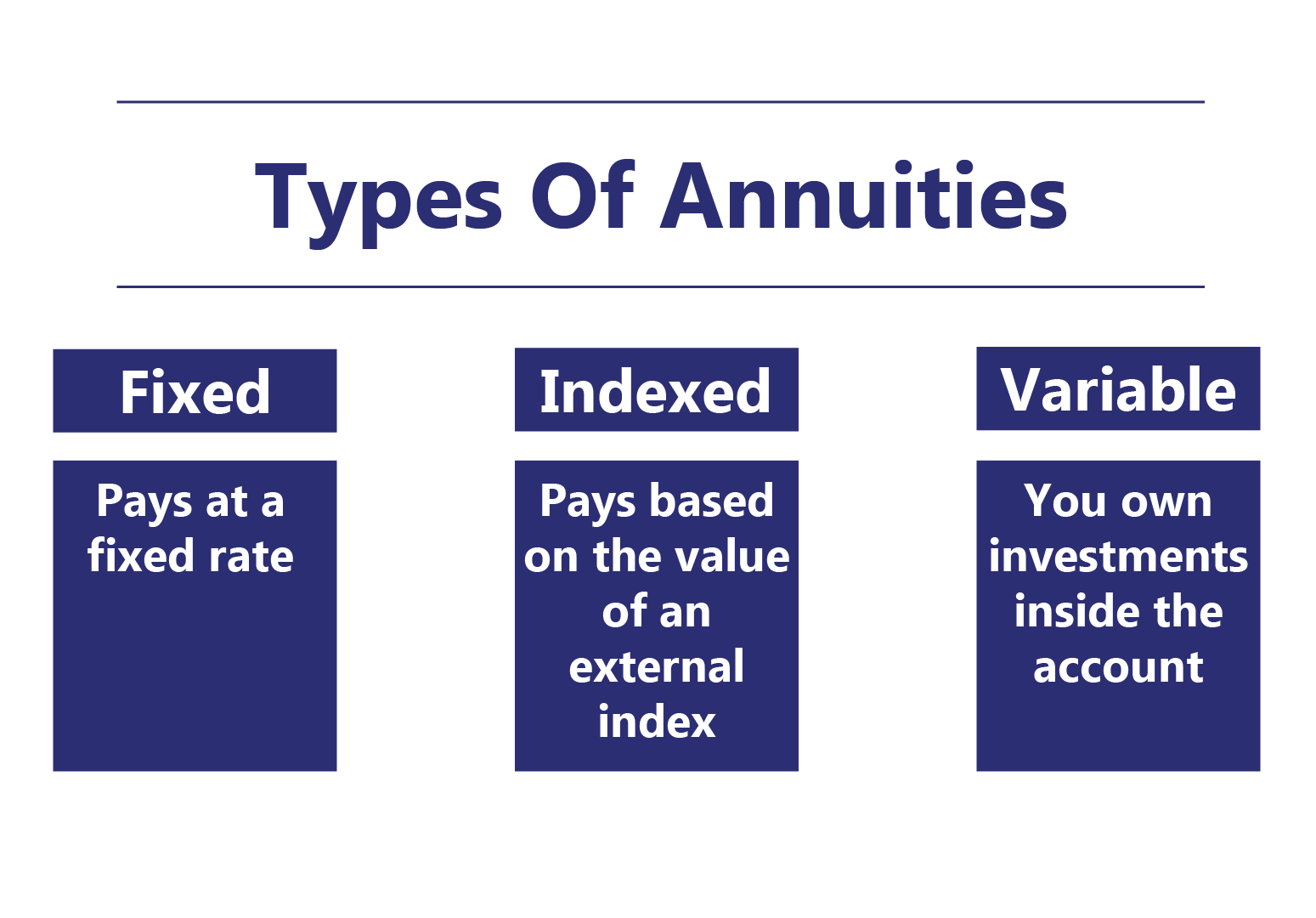

It is a contract that comes with an agreement describing certain assurances. Fixed annuities assure a minimal price of interest while you conserve and, if you choose life time income, a minimum regular monthly amount in retired life (annuity life insurance companies). Converting some or every one of your savings to revenue advantages (described as "annuitization") is a long-term decision

An assured life time annuity is a monetary product that promises to pay its proprietor earnings on a routine basis for the remainder of their life. Here's how ensured life time annuities job and exactly how to make a decision if one is best for you.

Surefire lifetime annuities are not government guaranteed yet may be covered by a state warranty fund. Guaranteed life time annuities, in some cases called ensured lifetime revenue annuities, are contracts offered by insurance companies. Their primary marketing point is that the buyer will never ever have to fret concerning lacking money as they age.

Annuity Yield

The purchaser of a guaranteed lifetime annuity pays the insurance provider either a lump amount of cash (a single-premium annuity) or a collection of costs (a multiple-premium annuity). In return, the insurance firm accepts give the buyerand their partner or one more individual, when it comes to a joint and survivor annuitywith a guaranteed earnings for life, regardless of for how long they live.

Some annuities, however, have a return-of-premium function that will certainly pay the annuity proprietor's beneficiaries any kind of cash that remains from the original premium. That can happen, as an example, if the annuity owner dies early into the contract. Some annuities likewise give a survivor benefit that works a lot like a life insurance plan.

The older the proprietor is when they begin getting revenue, the higher their settlements will be since their life span is shorter. In some feeling, a life time annuity is a wager in between the insurance provider and the annuity's proprietor. The insurer will certainly be the winner if the proprietor passes away before a specific factor, while the owner will appear in advance if they stun the insurance company by living longer than expected.

, the owner can begin to receive earnings right away.

In the meantime, the annuity will be in what's called its accumulation phase. Delaying revenue can permit the account to grow in worth, resulting in greater payments than with an instant annuity. The much longer that revenue is postponed, the greater the prospective accumulation. Immediate annuities have no accumulation stage.

Annuity Investing

A variable annuity, on the various other hand, will pay a return based on the financial investments that the proprietor has actually selected for it, generally one or more shared funds. When the payment phase starts, the proprietor may have an option of receiving set settlements or variable payments based upon the recurring efficiency of their financial investments.

Due to the fact that it is most likely to have a longer payout stage, a joint and survivor annuity will typically pay much less each month (or other time period) than a solitary life annuity.

Deferred Lifetime Annuity

, or other investments. They likewise have some downsides.

An assured lifetime annuity can provide revenue for the remainder of the owner's life. It can additionally be made to pay revenue to an enduring partner or various other person for the remainder of their life. Surefire life time annuities can begin their payments promptly or at some factor in the future.

Annuities can be costly, nonetheless, and, depending upon just how long the proprietor lives and obtains payments, might or may not show to be a good financial investment.

An instant annuity lets you promptly turn a lump amount of money right into an assured stream of earnings.

Your income is guaranteed by the business that issues the annuity. So, make certain the business you get your annuity from is monetarily audio. This info can be gotten from the leading independent rating agencies: A.M. Finest, Fitch, Moody's, and Criterion & Poor's. New York City Life has earned the highest possible ratings for financial strength presently awarded to united state

Annuities Chart

2 An income annuity can help shield against the danger of outliving your cost savings. The amount you obtain monthly is assured, and payments will proceed for as long as you live. 1 Bear in mind that revenue annuities are not fluid, and your premium is gone back to you only in the kind of revenue payments.

A fixed-rate annuity has a mentioned price of return and no loss of principal due to market recessions. It permits the proprietor to gain greater interest than bonds, money markets, CDs and other financial institution items. The financial investment expands tax-deferred, which indicates you will not need to pay taxes on the interest up until you withdraw cash from the annuity.

Ensured minimal price of return for a particular duration. Your investment will certainly expand tax-deferred until you take a withdrawal. There is no market risk with a dealt with annuity. Your principal is shielded and assured to build up at a set price. Set annuities offer some liquidity, typically 10% of the agreement's built up worth is available penalty-free on an annual basis if you are over 59, and some repaired annuities allow you to take out the interest on an annual basis.

Define Immediate Annuity

Annuities are developed to be lasting investments and regularly include fees such as income and death advantage biker charges and give up costs.

{kind=link}

Table of Contents

Latest Posts

Analyzing Fixed Vs Variable Annuity A Comprehensive Guide to Indexed Annuity Vs Fixed Annuity What Is Indexed Annuity Vs Fixed Annuity? Benefits of Immediate Fixed Annuity Vs Variable Annuity Why Choo

Breaking Down Choosing Between Fixed Annuity And Variable Annuity Key Insights on Your Financial Future What Is the Best Retirement Option? Pros and Cons of Various Financial Options Why Choosing the

Exploring the Basics of Retirement Options Key Insights on Your Financial Future Breaking Down the Basics of Investment Plans Features of Fixed Vs Variable Annuity Pros And Cons Why Choosing the Right

More

Latest Posts